Database

Academic Publications

(Click on title for abstract)

Fiscal Progressivity and the Time Consistency of Monetary Policy

This paper studies how progressive fiscal policy influences the conduct of monetary policy in tractable heterogeneous agent economies. A priori, progressive labor taxation is undesirable because it generates costly distortions. Nonetheless, it is an effective instrument to mitigate the inflation bias of monetary policy because it achieves a redistributive purpose. I analyze this commitment channel of progressive labor taxes through the lens of political conflicts. When agents vote on monetary and fiscal instruments, progressivity is decisive in curbing the inflation bias because it generates distributional conflicts: lower-productivity agents support higher labor taxes to preserve the consumption value of money holding and shift the burden of tax distortions to higher-productivity agents. Anticipating the reduction in inflation, agents unanimously desire to adopt a progressive fiscal system.

The Central Bank Strikes Back! Credibility of Monetary Policy under Fiscal Influence,

with Dmitry Matveev

How should independent central banks react if pressured by fiscal policymakers? We contrast the implications of two monetary frameworks: one, where the central bank follows a standard rule aiming exclusively at price stability against the other, where monetary policy additionally leans against fiscal influence. The latter rule improves economic outcomes by providing appropriate incentives to the fiscal authority. More importantly, the additional fiscal conditionality can enhance the credibility of the central bank to achieve price stability. We emphasise how the level and structure of government debt emerge as key factors affecting the credibility of monetary policy with fiscal conditionality.

Political Activism and the Provision of Dynamic Incentives,

with Russell Cooper

This paper studies the determination of income taxes in a dynamic setting with human capital accumulation. The goal is to understand the factors that support an outcome without complete redistribution, given a majority of relatively poor agents and the inability to commit to future taxes. All agents agree ex ante that limiting tax and transfers is beneficial but a majority favours large redistribution, ex post, at the time of the vote. In a political influence game, group activism limits the support for expropriatory taxation and preserves incentives. In some cases, the outcome corresponds to the optimal allocation under commitment.

Furor over the Fed: A President's Tweets and Central Bank Independence,

with Dmitry Matveev

We illustrate how financial market data are informative about the interactions between monetary and fiscal policy. Federal funds futures are private contracts that reflect investor's expectations about future monetary policy decisions. By relating price movements of these contracts with President Trump's tweets on monetary policy, we explore how financial market participants have perceived attempts by the President to influence monetary policy decisions. Our results indicate that market participants expected the Federal Reserve Bank to adjust monetary policy in the direction suggested by President Trump.

The Evolution of European Economic Institutions during the COVID-19 Crisis,

with Gregory Claeys

This article argues that the incomplete economic and institutional integration of the euro area has exposed the monetary union to increasing economic divergence, which could be deepened by the COVID-19 crisis. We discuss how monetary and fiscal measures implemented at the onset of the pandemic have contributed to mitigate the economic consequences of lockdowns, but provided limited insurance to narrow economic gaps across member countries. However, EU countries agreed on July 21, 2020 to develop, for the first time, countercyclical fiscal transfers financed by common debt issuance. We discuss the potential of this instrument to contribute to improve the resilience of the eurozone.

“Whatever It Takes” Is All You Need: Monetary Policy and Debt Fragility,

with Russell Cooper

The valuation of government debt is subject to strategic uncertainty. Pessimistic lenders, fearing default, bid down the price of debt, leaving a government with a higher debt burden. This increases the likelihood of default, thus confirming the pessimism of lenders. Can monetary interventions mitigate debt fragility? With one-period commitment to a state-contingent policy, the monetary authority can indeed overcome strategic uncertainty. Under discretion, debt fragility remains unless reputation effects are sufficiently strong. Simpler forms of interventions, such as an inflation target, cannot eliminate debt fragility.

Public Debt and Fiscal Policy Traps,

with Andrew Gimber

We present a theory linking the cyclicality of tax policy to inherited public debt. When debt is low, tax policy is countercyclical, in the sense that the government responds to low output by setting a low tax rate. Above a threshold level of debt, however, optimal tax policy becomes procyclical. This creates the possibility of self-fulfilling crises (“fiscal policy traps”), in which output is low because households expect high taxes, and the government sets high taxes because output is low. Our model suggests why highly indebted governments might implement procyclical tax policy even without facing high sovereign risk premia.

Working Papers & Work-in-Progress

(Click on title for abstract)

Monetary Communication and Credibility in a Multi-Sector Economy,

with Dmitry Matveev

Central banks increasingly communicate sectoral narratives about inflation. We propose a theory of monetary communication in a multi-sector New Keynesian economy in which the central bank privately observes aggregate and sector-specific fundamentals and chooses both a policy instrument and a public message. Under commitment, the optimal disclosure rule has a sharp threshold structure: the central bank always discloses aggregate conditions and, depending on sectoral elasticities, sizes, and price rigidities, either fully discloses both components or pools them into a single message. Without commitment, this rule is time-inconsistent, yielding a multi-sector analogue of the Barro-Gordon credibility problem. In a dynamic extension with unobservable policymaker types, reputation partially disciplines communication, but does not restore the commitment outcome. In an application to the euro area, the post-pandemic rise in price-adjustment frequency raises the likelihood that full sectoral disclosure is optimal.

Austria One Century Apart: Persistent Effects of Hyperinflation on Inflation Expectations,

with Natalia Garcia Soto, April 2026

Can the memory of past inflation shape how people form expectations about prices today? Using regional inflation data from Austria’s 1921–22 hyperinflation linked to quarterly consumer surveys (May 2020–Oct 2024), we document a persistent association between historical inflation exposure and contemporary inflation expectations: individuals from regions more exposed to the historical hyperinflation episode report higher inflation expectations, a century later. We further show that regional newspapers in historically high-inflation areas devote greater attention to inflation, suggesting that local media environments contribute to the intergenerational transmission of inflation attitudes. These findings indicate that the collective memory of major inflation episodes can durably shape expectation formation, with implications for managing heterogeneous regional responses during inflationary episodes.

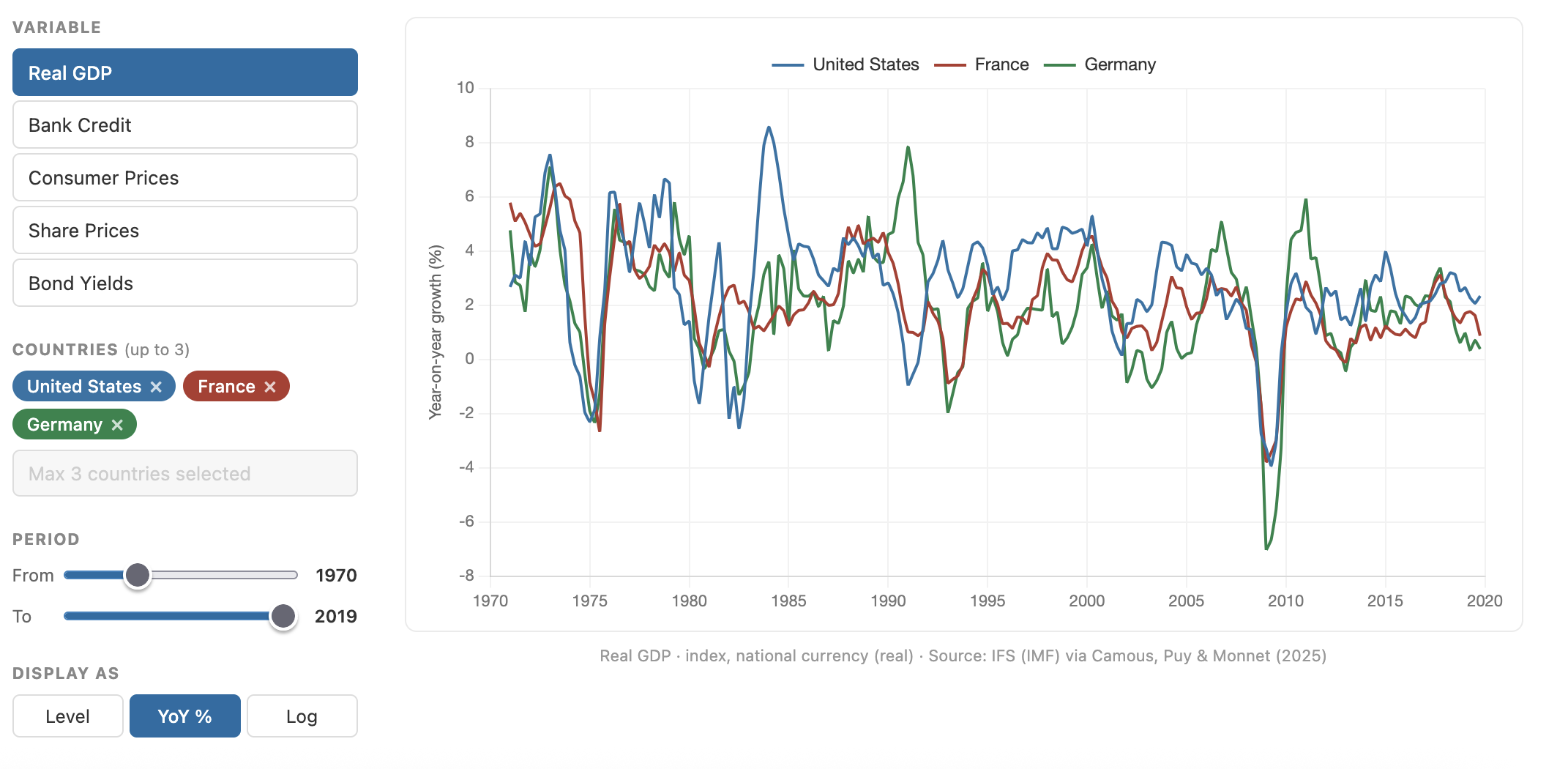

World Cycles Revisited: Diverging Trends in Prices and Quantities,

with Damien Puy and Eric Monnet, September 2025

We revisit evidence on world cycles using a new quarterly macro-financial dataset covering a broad set of countries from 1950 to the COVID-19 crisis. By filling historical data gaps, we show that previous studies overstated the influence of global factors on national GDP and credit fluctuations. Our central finding is a novel disconnect: asset prices have become increasingly synchronized under financial globalization, whereas output synchronization has remained low and stable. We propose a parsimonious model in which deeper financial integration raises risk-sharing and asset-price co-movement while encouraging riskier, less correlated production structures, thereby reconciling the observed patterns.

Evaluating the Financial Instability Hypothesis,

with Alejandro Van der Ghote

Historical accounts of financial crises emphasize the joint contribution of extrapolative beliefs and leveraged risk-taking to financial instability. This paper proposes a simple macro-finance framework to evaluate these views. We find a novel interplay between non-rational extrapolation and investment risk-taking that amplifies financial instability relative to a rational expectation benchmark. Furthermore, the analysis provides guidance on the design of cyclical policy interventions. Specifically, relative to a rational expectations benchmark, extrapolative expectations command tighter financial regulation, irrespective of whether the regulator shares these expectations.

License to Ease: Competition and the Conduct of Monetary Policy,

with Basile Grassi and Matteo Samarani

Monetary policy is transmitted through firms' pricing decisions, which are shaped by the competitive environment. Competition policy affects that environment through measures that shape the degree of product-market competition. We study the interaction between competition policy and monetary policy in a New Keynesian model with oligopolistic competition. A competition authority chooses the degree of product-market competition, trading off its benefits against a resource cost, while a central bank conducts monetary policy under discretion. In this environment, competition shapes firms' markups and strategic pricing incentives, thereby affecting both the slope of the Phillips curve and the long-run distortion that gives rise to inflation bias. We characterize the optimal institutional design when a benevolent planner delegates authority to both institutions and chooses their mandates. Our main result is that the optimal degree of central bank conservatism depends systematically on the effectiveness of competition policy. When competition can be promoted more effectively, equilibrium competition is higher, inflation bias is lower, and it is optimal to appoint a less conservative central bank. The analysis implies that competition policy and monetary policy should be jointly designed rather than in isolation.